![]()

seqcomp implements anytime-valid tools for the

sequential comparison of probabilistic forecasters, following the

framework of Choe and Ramdas (2024). Given two competing forecasters and

a sequence of binary or categorical outcomes, the package constructs

confidence sequences and e-processes for the running mean score

difference that are valid simultaneously at every point in time, without

requiring a pre-specified sample size or adjustment for repeated

monitoring.

The package provides:

All boundary computations (normal mixture, gamma-exponential mixture,

polynomial stitching) are implemented from scratch, with no dependency

on the confseq package.

The development version can be installed from GitHub:

# install.packages("pak")

pak::pak("alasgarliakbar/seqcomp")After CRAN acceptance:

install.packages("seqcomp")compare_forecasts() is the main entry point. It computes

pointwise scores, the running mean score difference, a confidence

sequence, and two one-sided e-processes in a single call.

library(seqcomp)

set.seed(1)

n <- 300

y <- rbinom(n, size = 1, prob = 0.55)

# Forecaster p has some signal; forecaster q always predicts 0.5

p <- ifelse(y == 1, 0.62, 0.38)

q <- rep(0.50, n)

out <- compare_forecasts(

p = p,

q = q,

y = y,

scoring_rule = "brier"

)

tail(out[, c("t", "estimate", "lower", "upper", "e_pq", "e_qp")])

#> t estimate lower upper e_pq e_qp

#> 295 295 0.1056 0.07129320 0.1399068 2681618 2.220446e-16

#> 296 296 0.1056 0.07140910 0.1397909 2824574 2.220446e-16

#> 297 297 0.1056 0.07152422 0.1396758 2975161 2.220446e-16

#> 298 298 0.1056 0.07163857 0.1395614 3133784 2.220446e-16

#> 299 299 0.1056 0.07175215 0.1394478 3300873 2.220446e-16

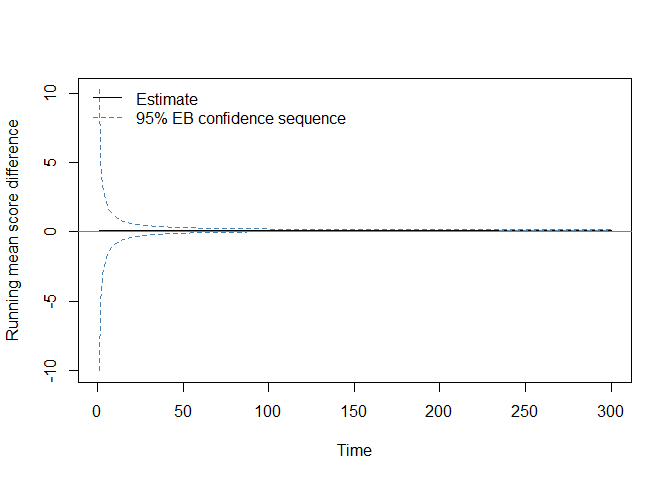

#> 300 300 0.1056 0.07186498 0.1393350 3476882 2.220446e-16The column estimate is the running mean score difference

\(\hat{\Delta}_t = t^{-1}\sum_{i=1}^t (S(p_i,

y_i) - S(q_i, y_i))\). Positive values favour p;

negative values favour q. The columns lower

and upper are the empirical Bernstein confidence sequence

bounds. The columns e_pq and e_qp are the two

one-sided e-process values; the two-sided rejection threshold at level

alpha = 0.05 is 2 / 0.05 = 40.

plot(

out$t, out$estimate,

type = "l",

ylim = range(c(out$lower, out$upper, 0), finite = TRUE),

xlab = "Time",

ylab = "Running mean score difference"

)

lines(out$t, out$lower, lty = 2, col = "steelblue")

lines(out$t, out$upper, lty = 2, col = "steelblue")

abline(h = 0, col = "gray50")

legend(

"topleft",

legend = c("Estimate", "95% EB confidence sequence"),

lty = c(1, 2),

col = c("black", "steelblue"),

bty = "n"

)

Two scale conventions are used throughout, following Choe and Ramdas

(2024) exactly. Theorem 1 (Hoeffding CS) requires \(|\hat{\delta}_i| \leq c\), so

c = 1 is used for Brier or spherical score differences in

\([-1, 1]\). Theorems 2 and 3

(empirical Bernstein CS and e-process) require \(|\hat{\delta}_i| \leq c/2\), so

c = 2 is used for the same score differences.

compare_forecasts() applies these conventions

automatically. They differ from the Python comparecast

package, which applies the Theorem 2/3 convention throughout.

compare_forecasts() is a convenience wrapper. The

underlying functions can be called directly for finer control:

scores_p <- brier_score(p, y)

scores_q <- brier_score(q, y)

cs <- cs_bernstein(scores_p, scores_q, alpha = 0.05, c = 2)

ep <- eprocess(scores_p, scores_q, alpha = 0.05, c = 2)The statistical methods in seqcomp are based on:

The package was developed as part of a bachelor’s thesis at the Vienna University of Economics and Business (WU Vienna).

If this package is used in published work, please cite the package itself and the following papers:

citation("seqcomp")Choe, Y. J. and Ramdas, A. (2024). Comparing Sequential Forecasters. Operations Research, 72(4), 1368–1387. https://doi.org/10.1287/opre.2021.0792

Howard, S. R., Ramdas, A., McAuliffe, J. and Sekhon, J. (2021). Time-uniform, nonparametric, nonasymptotic confidence sequences. The Annals of Statistics, 49(2). https://doi.org/10.1214/20-AOS1991

Howard, S. R., Ramdas, A., McAuliffe, J. and Sekhon, J. (2020). Time-uniform Chernoff bounds via nonnegative supermartingales. Probability Surveys, 17, 257–317. https://doi.org/10.1214/18-PS321

Ramdas, A., Grünwald, P., Vovk, V. and Shafer, G. (2023). Game-theoretic statistics and safe anytime-valid inference. Statistical Science, 38(4), 576–601. https://doi.org/10.1214/23-STS894

Waudby-Smith, I., Arbour, D., Sinha, R., Kennedy, E. H. and Ramdas, A. (2024). Time-uniform central limit theory and asymptotic confidence sequences. The Annals of Statistics, 52(6). https://doi.org/10.1214/24-AOS2408