[dpr]mvss: multivariate subgaussian stable

distributions[pr]mvlogis: multivariate logistic distributionsThe goal of mvpd is to use product distribution theory

to allow the numerical calculations of specific scale mixtures of the

multivariate normal distribution. The multivariate subgaussian stable

distribution is the product of the square root of a univariate positive

stable distribution and the multivariate normal distribution (see Nolan

(2013)).

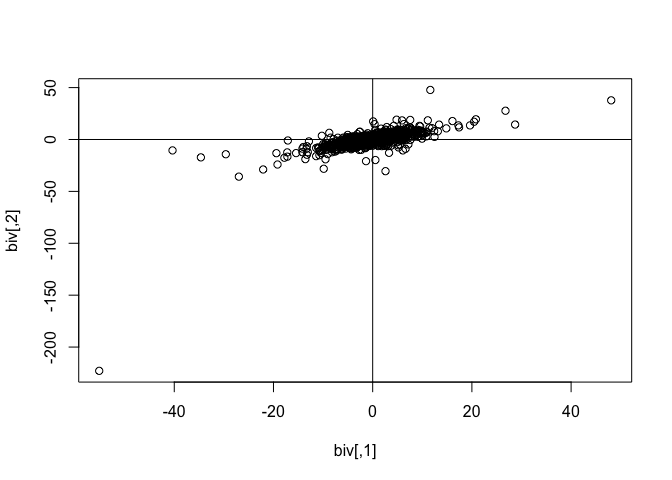

Generate 1000 draws from a random bivariate subgaussian stable distribution with alpha=1.71 and plot.

library(mvpd)

set.seed(2)

## basic example code

biv <- rmvss(n=1e3, alpha=1.71, Q=matrix(c(10,7.5,7.5,10),2))

head(biv)

#> [,1] [,2]

#> [1,] 3.17465324 4.122869

#> [2,] -3.26707008 -1.366920

#> [3,] -5.82800100 1.831774

#> [4,] -2.02463359 -3.749701

#> [5,] 0.01294963 3.042960

#> [6,] 1.73029594 3.812420

plot(biv); abline(h=0,v=0)