![]()

![]()

![]()

![]()

dfms provides efficient estimation of Dynamic Factor Models

in R via the EM Algorithm. Factors are assumed to follow a stationary

VAR process of order p. Estimation can be done in 3

different ways following:

Doz, C., Giannone, D., & Reichlin, L. (2011). A two-step estimator for large approximate dynamic factor models based on Kalman filtering. Journal of Econometrics, 164(1), 188-205. doi:10.1016/j.jeconom.2011.02.012

Doz, C., Giannone, D., & Reichlin, L. (2012). A quasi-maximum likelihood approach for large, approximate dynamic factor models. Review of Economics and Statistics, 94(4), 1014-1024. doi:10.1162/REST_a_00225

Banbura, M., & Modugno, M. (2014). Maximum likelihood estimation of factor models on datasets with arbitrary pattern of missing data. Journal of Applied Econometrics, 29(1), 133-160. doi:10.1002/jae.2306

The default is em.method = "auto", which chooses

"BM" following Banbura & Modugno (2014) with missing

data or mixed frequency, and "DGR" following Doz, Giannone

& Reichlin (2012) otherwise. Using em.method = "none"

generates Two-Step estimates following Doz, Giannone & Reichlin

(2011). This is extremely efficient on bigger datasets. PCA and Two-Step

estimates are also reported in EM-estimation. All methods support

missing data, but em.method = "DGR" does not model them in

EM iterations.

The package is now at a 1.0.0 release and includes

news() for Banbura and Modugno (2014) style news

decomposition of forecast updates.

dfms provides a simple, numerically robust, and

computationally efficient implementation of (linear Gaussian) Dynamic

Factor Models for R, allowing straightforward application to time series

dimensionality reduction, forecasting, and nowcasting tasks. It is based

on efficient C++ code, making dfms orders of magnitude faster

than other packages that can be used to fit dynamic factor models such

as MARSS, or

nowcasting

and nowcastDFM

geared to mixed-frequency nowcasting applications - which dfms

now also supports. For large-scale nowcasting models the DynamicFactorMQ

class in the statsmodels Python library is likely the best

implementation - see the example

by Chad Fulton.

The dfms package is not intended to fit more general forms of

the state space model like MARSS.

# CRAN

install.packages("dfms")

# Development Version

install.packages('dfms', repos = c('https://ropensci.r-universe.dev', 'https://cloud.r-project.org'))library(dfms)

# Fit DFM with 6 factors and 3 lags in the transition equation

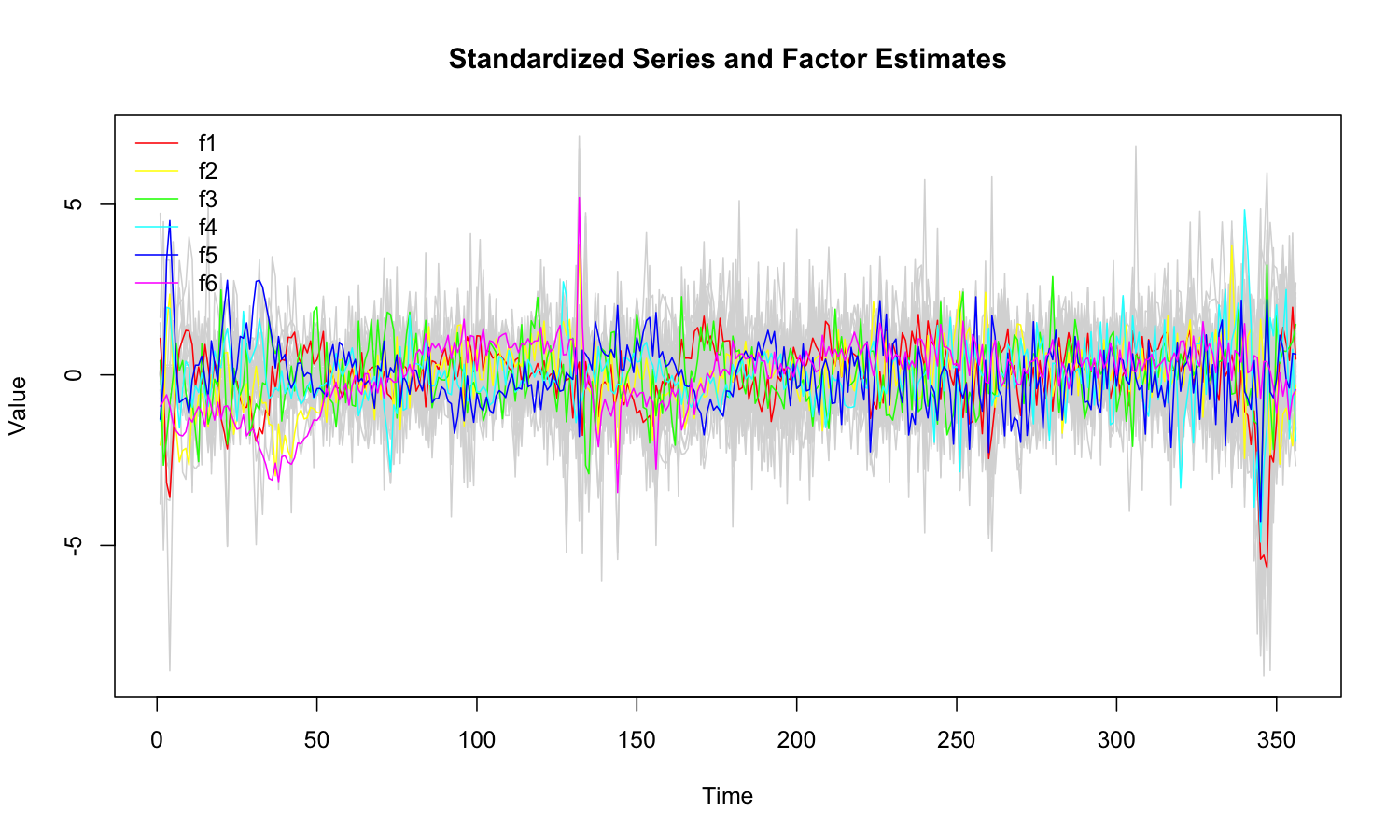

mod <- DFM(diff(BM14_M), r = 6, p = 3) ## Converged after 32 iterations.# 'dfm' methods

summary(mod)## Dynamic Factor Model: n = 92, T = 356, r = 6, p = 3, %NA = 25.8366

##

## Call: DFM(X = diff(BM14_M), r = 6, p = 3)

##

## Summary Statistics of Factors [F]

## N Mean Median SD Min Max

## f1 356 -0.1189 0.4409 4.0228 -22.9164 7.8513

## f2 356 -0.4615 -0.3476 2.9201 -9.0973 10.7003

## f3 356 -0.0173 0.0377 2.2719 -8.5067 7.3009

## f4 356 -0.007 -0.1338 1.9378 -9.5052 9.3673

## f5 356 0.237 0.1091 2.0857 -8.7252 9.6715

## f6 356 -0.8361 -0.304 3.1406 -11.6611 15.4897

##

## Factor Transition Matrix [A]

## L1.f1 L1.f2 L1.f3 L1.f4 L1.f5 L1.f6 L2.f1 L2.f2 L2.f3

## f1 0.53029 -0.53009 0.367302 0.04607 -0.06351 0.10310 0.02457 0.11673 -0.12638

## f2 -0.28380 0.07421 -0.032292 0.29741 -0.10094 0.21989 0.09958 -0.09149 0.06708

## f3 0.17607 0.12979 0.378798 -0.06662 -0.12236 0.06685 -0.08068 0.09101 -0.22232

## f4 0.02711 0.08936 0.004643 0.37159 0.12100 -0.02763 0.01234 -0.05147 0.02195

## f5 -0.26227 -0.03469 -0.046294 0.12712 0.26847 0.03141 0.06400 0.01971 0.04806

## f6 0.08251 0.17619 -0.013374 -0.08731 -0.03875 0.27812 -0.01662 0.04877 0.02279

## L2.f4 L2.f5 L2.f6 L3.f1 L3.f2 L3.f3 L3.f4 L3.f5 L3.f6

## f1 0.23135 0.117184 0.21941 0.18478 0.02259 -0.03719 -0.07236 -0.03026 -0.12606

## f2 -0.09768 -0.043057 0.08489 0.21107 0.16261 0.03057 0.04835 0.12249 0.13357

## f3 0.09799 -0.060666 -0.18028 -0.02773 0.01798 0.10143 -0.12420 0.04207 -0.07011

## f4 0.01266 0.050912 0.05144 -0.05601 0.04665 0.05710 -0.11412 -0.05680 -0.01609

## f5 -0.03965 -0.009952 -0.18471 0.08332 -0.04640 -0.02047 0.02458 0.16397 0.07820

## f6 0.01163 -0.100859 0.07152 0.00792 0.06071 0.11381 0.02520 -0.17897 0.30328

##

## Factor Covariance Matrix [cov(F)]

## f1 f2 f3 f4 f5 f6

## f1 16.1832 -0.4329 0.2483 -0.8224* -1.7708* 0.7702

## f2 -0.4329 8.5272 0.0051 0.2954 -0.2114 4.2080*

## f3 0.2483 0.0051 5.1614 -0.1851 -0.3979 0.2979

## f4 -0.8224* 0.2954 -0.1851 3.7550 0.4344* 0.2211

## f5 -1.7708* -0.2114 -0.3979 0.4344* 4.3503 -1.9785*

## f6 0.7702 4.2080* 0.2979 0.2211 -1.9785* 9.8634

##

## Factor Transition Error Covariance Matrix [Q]

## u1 u2 u3 u4 u5 u6

## u1 7.2142 0.1151 -0.8208 -0.4379 0.4110 -0.1206

## u2 0.1151 4.8724 0.1076 -0.1438 0.1418 0.1759

## u3 -0.8208 0.1076 4.0584 -0.0788 0.0163 0.0038

## u4 -0.4379 -0.1438 -0.0788 3.0003 0.2562 0.0243

## u5 0.4110 0.1418 0.0163 0.2562 2.8410 -0.1031

## u6 -0.1206 0.1759 0.0038 0.0243 -0.1031 2.9284

##

## Summary of Residual AR(1) Serial Correlations

## N Mean Median SD Min Max

## 92 -0.0644 -0.1024 0.2702 -0.5113 0.6674

##

## Summary of Individual R-Squared's

## N Mean Median SD Min Max

## 92 0.4556 0.4069 0.3041 0.0112 0.9989plot(mod)

as.data.frame(mod) |> head()## Method Factor Time Value

## 1 PCA f1 1 0.8445713

## 2 PCA f1 2 0.5259228

## 3 PCA f1 3 -1.2107116

## 4 PCA f1 4 -1.5399532

## 5 PCA f1 5 -0.4631786

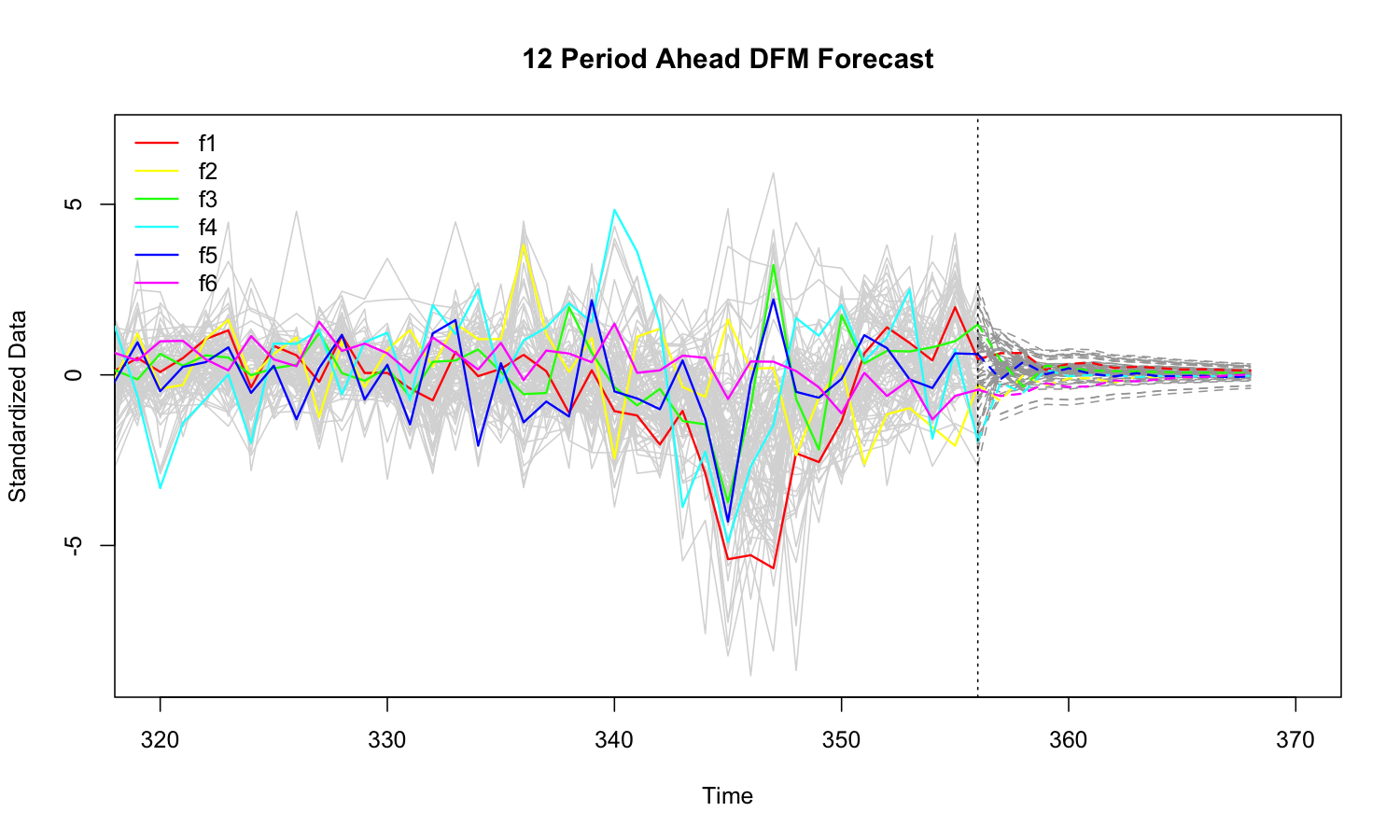

## 6 PCA f1 6 0.2399304# Forecasting 12 periods ahead

fc <- predict(mod, h = 12)

# 'dfm_forecast' methods

plot(fc, xlim = c(320, 370))

as.data.frame(fc) |> head()## Variable Time Forecast Value

## 1 f1 1 FALSE 4.179331

## 2 f1 2 FALSE -1.368577

## 3 f1 3 FALSE -12.845157

## 4 f1 4 FALSE -14.562265

## 5 f1 5 FALSE -7.791254

## 6 f1 6 FALSE -1.254970